The Good, the Bad, and the Ugly

A rundown of opinions on the House reconciliation bill

Happy June, Happy Pride, Happy Gemini season, and happy almost summer! Today, I’m (finally) providing some deeper thoughts on the higher ed portion of the House reconciliation bill that passed last month. To get a rundown of what’s in the bill, you can refer back to my posts that run down the student aid and accountability policy changes made by the bill.

A note: I’m calling out the most major pieces of the bill here. There are smaller changes here and there that I like and don’t like, but I’m mostly focusing on the big bangs.

Another note: In addition to doing some contracting work, I’m also traveling through mid-August, so my posts may be a bit intermittent, though I do intend to get back to my post-a-week cadence, with regular posts for paid subscribers filled with musings that are even more unfiltered than what you find here.

The Good

There are some really solid changes made in this bill, especially on the accountability side of the ledger. Though it’s somewhat convoluted, I am pleased as punch that that there is risk sharing in this bill, and that the schools that are projected to get the steepest fines are those that have long been scrutinized for taking advantage of students (mostly by Democrats!) and that Liberty Freaking University is number 3 on the list. I can’t stomach all of the culture war sludge that has permeated both the left and the right in recent years, and it is refreshing to see House REPUBLICANS vote to hold mostly for-profits and other shyster-y schools (this is a technical term) to account in statute.

Unfortunately, talk around town is that risk sharing is the most likely provision to be jettisoned by the Senate, but may as well give credit where it’s due.

I also have to say that I don’t hate a lot of the changes to the loan program. I am out of step with a lot of what liberals are saying publicly (though many agree with me privately) in the fact that I really, really like the new aggregate loan limits, including the elimination of Graduate PLUS and new limits on graduate debt. Schools have been able to make a whole lot of money for a long time due to a combination of unlimited borrowing for graduate students and zero accountability for graduate program outcomes. This has absolutely buried my generation (millennials) in particular in debt, and whenever you hear about someone buried in hundreds of thousands in debt and high interest, 9 times out of 10 it’s because they made a real bad decision when it came to borrowing for graduate school. As I stated in a paid-only post recently, I find it, let’s say, amusing, that borrower advocates have come out strongly against limiting graduate borrowing while also screaming that people are buried in predatory debt. Nothing sounds more predatory to me than unlimited borrowing for a low-value product, but what do I know, I’m a neoliberal shill in the pocket of industry (or so I’ve been told).

On the Parent PLUS side, I am also in favor of loan limits, though I think this could be improved by also imposing more rigorous credit standards. Right now, you can get a $50,000 per year PLUS loan on an income of $20,000, even if you’re underwater on other debt. It’s absolutely unconscionable, and while I appreciate that some schools enroll higher-need populations, those students shouldn’t have to enroll at the expense of their parent’s financial stability. The school needs to be accountable for providing an affordable education, ensuring the borrower completes their program, and offering a credential of value. The fact that this is controversial is absolutely wild to me.

Finally, I am all in favor for simplifying repayment options. A Standard plan and an IDR plan make sense, and I do like increasing the Standard Plan term as a borrower takes on more debt. I also don’t hate that there is a minimum payment that isn’t $0. There is a tension between offering a $0 payment (offered by most IDR plans now) and requiring some payment to keep the borrower financially engaged in repayment. It is very easy for a borrower to fall out of IDR and roll right through delinquency into default right now, and keeping a borrower either in an auto-debit or at least in contact with their servicer on a monthly basis will help keep borrowers engaged in the repayment system. While the House bill requires a $10 per month minimum, the currently policy for defaulted borrowers to rehabilitate a loan to get it back in good standing is $5 per month, and I don’t see why these policies shouldn’t be aligned. Though I think that the payment ramp-up starts too low on the income spectrum (where you pay more than $10 if you make $20,000 per year), I don’t think requiring a minimal payment is a bad thing.

Finally, it is absolutely and completely necessary to provide FSA with substantial funding to implement the policies in this bill. $500M each year for the next two years is honestly not a ton considering FSA has been effectively flat funded since fiscal year 2022 and the White House and appropriations committees are highly unlikely to boost spending for FSA given what I’ll call the uh, government fiscal orientation of the current Congress and White House.

The Bad

Sigh. Now we dig into the things I hate, and topping the list here are cuts to Pell and eliminating subsidized loans. The purchasing power of the Pell Grant - which currently maxes out at $7,395 per year, which doesn’t even cover tuition at most colleges. It’s not enough to support low-income students, and it’s honestly unconscionable to make such massive cuts to what should be the cornerstone of higher education affordability. Add to that the elimination of subsidized loans - which cover the accrued interest on a loan for as long as a borrower is enrolled - and what are we even doing here? It feels cruel and unnecessary, especially with other provisions in the bill that are designed to push colleges to get borrowers to complete on time.

I also think it’s silly to get rid of economic hardship and unemployment deferments, especially because the RAP requires a $10 monthly payment. Combine them into one deferment if you want to simplify things, but again, it just seems cruel to get rid of these programs, especially because it barely saves any money and the house overshot their target by $20ish billion.

The Ugly

And by ugly, I mean a mess. These provisions are ones that, upon reading, I got anxious thinking implementing, even though I don’t need to work on the implementation anymore.

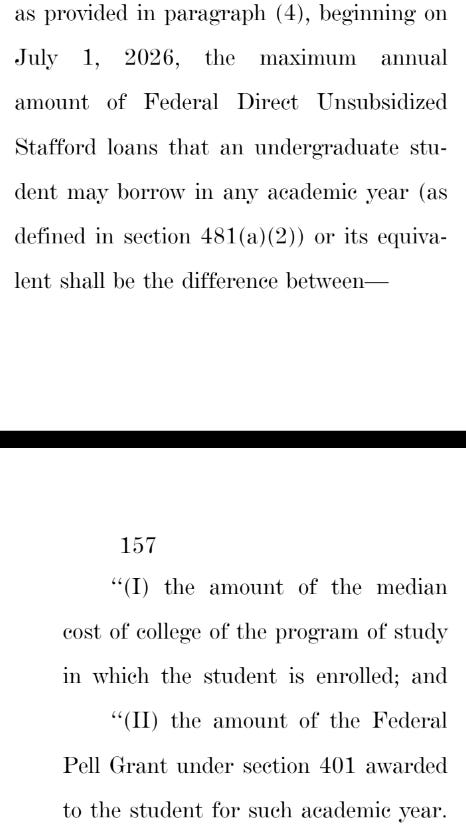

Top of the list here is the annual loan limit, which, as a reminder, would be based on the median cost of attendance for a borrower’s program of study across all colleges. More specifically:

I cannot describe to you how unnecessary, complicated, and NOT SIMPLE this will be in practice. The intention here seems to be to get schools to charge students based on the cost of educating them (with the idea that it’s more expensive to educate an engineer than an English major). But let’s be real, there is not that much of a cost differential at the associate and bachelor’s degree level, and it is going to lead to so much complexity it makes me want to vomit. Let me just walk through a few of the reasons I freaking hate this policy:

In a time when financial aid award letters have drawn bipartisan scrutiny for being too nebulous and not specific enough, this policy just compounds that problem. A school will have to either add a question to its application that requires a student to declare a major, place everyone into a general studies program, or set its own loan limit for its students. This won’t be consistent across schools, so it will be hard to compare award letters, and financial aid offices will field thousands of questions from confused students and parents. Fun stuff.

Students change their major and they don’t do it when it neatly coincides with loan disbursements. Let’s imagine a borrower receives a loan in the fall then changes their major to a program with a lower median cost than the previous program. Would the school have to take back some of the disbursement for the fall semester, thus creating a bill for the student partway through the semester that they then need to figure out how to pay? Would they just be able to reduce the disbursement for the spring semester? If so, how would the borrower cover the higher balance that they didn’t anticipate in spring? What happens if the student drops out? And this is just for the schools that use a traditional calendar; I shudder to think what schools who use clock hours and quarters will have to deal with. Basically any way this shakes out, it’s going to result in an avalanche of return of Title IV (R2T4) calculations, which require a ton of work from financial aid offices and are so complex and thorny that numerous groups have failed to even come up with recommendations to improve the process over the years. Schools will have to hire a boatload of folks just to process R2T4s (so much for administrative bloat that Republicans love complaining about), and many students will be caught off guard when they find out that what they thought was an academic decision turns out to have immediate financial consequences.

I get that the goal here is to get colleges to try and reduce their program costs but this is a truly roundabout way of doing that, and the provision allowing schools to set their own loan limits completely undermines that so… what are we doing here?

This policy requires a massive new data collection, and I’m not sure if you’ve heard, but the Department of Education has been cut in half staffing-wise and its statistical arm has been completely gutted. Soooooooo… not sure how well that new data collection is going to go, or even when it would be implemented (but sure as hell isn’t July 1, 2026).

This doesn’t need to be totally scrapped. Leave it in place for graduate and certificate programs, where a student enrolls in a specific program and where the costs are far more divergent. But this is just foolishness for the bulk of students. Set a blanket loan limit - say, $7,000 or $8,000 per year - and call it a day.

The other “blech” criticisms I have are more broad. I just think Workforce Pell is going to be a mess, especially in regards to assessing program quality. And honestly, enforcement of basically every part of this bill is going to be extremely challenging, especially with the gutting of the Department. I’m also not sure how this interacts with the curtailing of Secretarial authority in this bill and what legal challenges will be presented by a Secretary attempting to make these policies enforceable by providing guidance, then being sued by institutions who don’t like the guidance and saying the Secretary is overstepping.

Finally, the implementation timeframes on this thing are just not workable. Even with the money, FSA (and the Department, who has an appreciable part of this with the need to regulate on parts of it) can’t get all of this (or frankly even half of this) done in a year.

That’s all for now. Looking forward to hearing folks thoughts, and I’m very much interested in seeing what the Senate comes out with in the coming weeks. Until next week! I appreciate you.

Thanks so much for breaking this stuff up, Colleen. To me, the way it’s written, is that Congress has no idea what it’s like to be a young kid in college, thinking your going X program, and then switching to Y, and then, wait a minute, let’s throw Z in there, too. This will be a nightmare for FAAs everywhere, and it will take ED the entire year just to get the policy surrounding this out. Shout out to the FSA staff we left behind, who are doing double and triple duty.