Massive Changes are Coming for Student Loans

Reconciliation is about to remake the American higher education system

Just in case we weren’t already drinking from a fire hose with all of the changes being made to higher education, today, House Republicans published a 103 page bill that will completely remake the postsecondary landscape. Upon waking up this morning, I looked forward to hitting send on my previously drafted post and doing some yard work in sunny Asheville, NC. But alas, I (and most other people in the higher ed space) have spent the last 10ish hours frantically reading the bill, cross referencing statutory text, and tip tapping away on our compies and phones, asking our genius friends and colleagues questions on interpretation and occasionally screaming into the void.1

The changes made by the Student Success and Taxpayer Savings Plan can be sorted into four broad categorizes: aid eligibility, loan repayment, college accountability, and Education Department authority and funding. In this post, I’ll cover the first two areas and will follow up with the other two in a post later this week. This is my first read and I know for a fact that I’m missing things and will undoubtedly get some things wrong, so please be kind. I look forward to paid subscribers highlighting what I missed in the comments and for a very lively conversation in the paid subscriber chat.

Aid Eligibility

This bill drops several bombs when it comes to the aid available to college students, especially when it comes to student loans. For the most part, these changes would become effective on July 1, 2026. The bill:

Eliminates subsidized loans, which are currently available to undergraduate students with financial need, which is their family’s financial resources as defined by the FAFSA (i.e. the Student Aid Index, or SAI, formerly called the Expected Family Contribution, or EFC) subtracted from the the total cost of attendance at a school (e.g. tuition, fees, living expenses, books, etc). Without subsidized loans, interest would accrue on every single student loan from the date it is disbursed. This will significantly increase student loan balances for borrowers upon leaving school.

Eliminates Graduate PLUS loans. These loans do not currently have an annual or aggregate limit and are the primary way graduate students pay for school today, given they can “only” borrow $20,500 per year from the only other federal loan available to graduate borrowers, the unsubsidized Stafford loan.

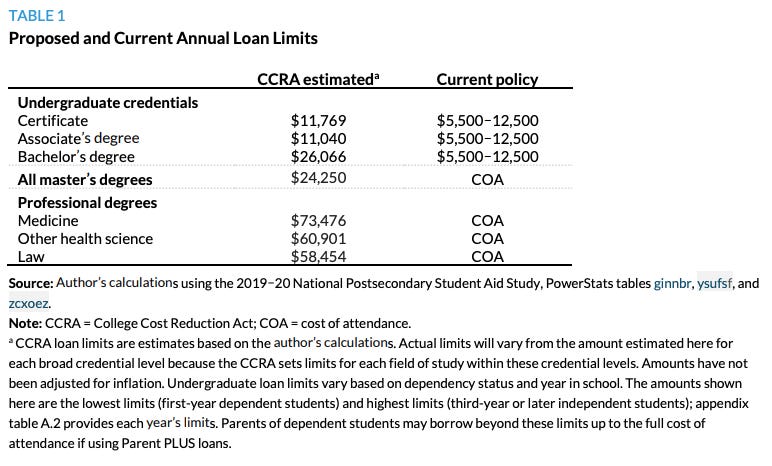

Changes the annual loan limit for undergraduate and graduate borrowers to be the difference between the median cost of borrower’s the program of study (which includes degree and field/major) and the amount received in a Pell Grant. Because this was included in the College Cost Reduction Act (CCRA), introduced last year by Virginia Foxx (R-NC), Jason Delisle and Kristin Blagg have published very helpful analyses on what these annual limits might look like across different programs.

Modifies the annual limit for Parent PLUS borrowers to the cost of attendance minus the student’s annual loan limit.

Modifies the aggregate maximum amounts that student and parent borrowers can take out, with the maximum being:

$50,000 for undergraduates (down from $57,500 currently),

$100,000 for graduate students (down from $138,500 in unsubsidized loans currently, though graduate students can essentially borrow as much as they need over time because of Graduate PLUS),

$150,000 for professional students (again reduced from the unlimited amount allowed today due to Graduate PLUS),

$50,000 for Parent PLUS loans (down from the unlimited amount allowed today), and

$200,000 lifetime aggregate maximum, which is set regardless of if a borrower pays off or receives forgiveness for a portion of their debt (e.g. if a borrower hits their $200K limit and pays off half of it, they cannot borrow more just because they paid off $100K… they’re done borrowing federal loans forever).

Requires students to borrow their up to their annual loan limit before a parent can take a PLUS Loan.

Creates “Workforce Pell Grants” which are sometimes referred to as “short-term Pell” and provide Pell Grants to students enrolling in programs that run between 8 and 14 weeks.

Eliminates federal aid eligibility for most non-citizens in the U.S. who are here on asylum (among other statuses).

Keeps current loan eligibility for currently enrolled borrowers, but only for the “expected time to credential,” which is capped at 3 years.

A quick and dirty rundown

These are massive reforms that will change the way that students and colleges interact in the higher education landscape. I think the modifications to annual borrowing limits will lead to undergraduates borrowing more (because they’ll have access to higher loan limits each year) and to graduate students borrowing far less.

The way annual loan limits are currently structured don’t make sense, so I’m not totally against reforming them, but I have a ton of questions about how the new annual loan limits will work practically. For example, most undergraduate students don’t enroll in college with a declared major, but if an annual loan limit needs to be based on borrowers’ program of study, how will borrowers know how much they will be able to take out each year? And how does that work if they change their major? While I get the premise, the implementation is a nightmare, and it would probably be better just to set a level in statute based on current costs rather than establish oba highly variable rate for each borrower depending on what they study.

I also have questions about how the f this will work for graduate programs, particularly in high-need fields like medicine, where the average borrower finishes their studies with over $200K in debt from medical school alone. I think it is very necessary to limit graduate borrowing (and to hold graduate programs accountable for their outcomes), but it’s unclear to me how schools are going to make all of this work given graduate programs (read: the debt borrowed by students in graduate programs) keep a lot of schools afloat.

The Parent PLUS limit is also kind of wild, and you can expect a whole lot of schools - especially higher-cost private schools - to lose their ever-loving shit over this. The Obama administration tried to draw some very reasonable limits around Parent PLUS in the past and quickly walked it back because the HBCUs lobbied hard against it, and I’m curious if Congress will similarly cave. I’m not averse to changing PLUS rules given their negative impact on intergenerational debt, but like many other parts of these changes, I struggle to see how colleges will make all of this work.

Loan Repayment

This bill will totally change how student loans are repaid, not just for new borrowers, but for current ones.

For new borrowers as of July 1, 2026 (in most cases anyway), the bill:

Provides borrowers with only two repayment plan options: a Standard Plan and new income-driven repayment plan, the Repayment Assistance Plan (RAP). The Standard Plan would provide borrowers with a fixed monthly payment amount over a given repayment term based on how much the student borrowed:

10 years for balances less than $25,000,

15 years for balances between $25,000 and $50,000,

20 years for balances between $50,000 and $100,000, and

25 years for balances over $100,000.

The Repayment Assistance Plan (RAP) would be the only IDR plan available. Borrowers would be enrolled into the Standard Plan if they didn’t choose the RAP, but once in the RAP, borrowers wouldn’t be able to move out of it unless they borrowed more loans. On Standard or RAP, borrowers could pay down their loans faster without penalty. The RAP’s terms are as follows:

Minimum monthly payment amount is $10

30 year maximum repayment term before the balance is forgiven

Requires on-time payments of the full amount due in order for a payment to qualify toward that 30 year payment term.

Months in economic hardship deferment would count toward RAP forgiveness.

Monthly payments are based on the adjusted gross income (AGI) of the borrower and their spouse (or just the borrower in cases where they are married and file separately).

Borrowers in RAP would get a reduction in their monthly payment of $50 per dependent child

If a borrower’s interest is not paid down by their monthly payment, it would be forgiven (this would prevent negative amortization, where a loan’s balance grows due to unpaid interest),

If a borrower’s payment reduces principal by less than $50, the principal would be reduced by the same amount of principal paid by the borrower (e.g. if you pay down $40 of principal, the government would write off an additional $40 of principal).2

For new loans as of July 1, 2025:

borrowers can no longer use an unemployment or economic hardship deferment,

Forbearance is limited to 9 months within a 24 month period, and

Forbearances associated with medical and dental residencies will have interest subsidized for first 4 years.

For borrowers with loans made before July 1, 2026 (i.e. current borrowers), the bill:

Allows borrowers to continue to use the current version of the Standard, Graduated, Extended, and Alternative repayment plans. Borrowers can’t use the new Standard Plan.

For all student borrowers, eliminates the Income Contingent Repayment (ICR) Plan and the plans created off ICR statute - Pay As You Earn Plan (PAYE) and Saving for A Valuable Education (SAVE) - and puts borrowers enrolled in those plans into IBR.

Reverts the Income-Based Repayment (IBR) plan to its original terms, requiring borrowers pay 15% of their discretionary income (rather than 10%). It also removes the IBR partial financial hardship cap so that borrowers can participate in IBR even if their calculated payment amount exceeds their Standard payment amount and sets IBR forgiveness at 20 years for borrowers with undergraduate loans and 25 years for borrowers with graduate loans.

Allows Parent PLUS borrowers to use ICR, but only if they are enrolled in ICR as of the day before the bill is signed.

There are also some provisions that apply to both new and old borrowers.

Borrowers who default will be able to rehabilitate out of default twice, rather than once, which is current law.

The most recent Borrower Defense to Repayment and Closed School Discharge regulations are repealed (which were never implemented anyway).

Removes residency programs as qualifying public service jobs for PSLF.

Simplification Schmimplification

This is, all in all, a pretty overwhleming rewrite of student loan repayment, including for current borrowers. While simplification is always a stated goal, that’s never how things end up in actuality.

When you bifurcate eligibility (e.g. loans made before July 1, 2026 vs after), shit gets complicated very fast. This bill tries to solve for this by forcing as many people as possible into the new borrower terms by stating that, if you borrow after July 1, 2026, you only qualify for the new repayment rules. By my read, in this scenario, it seems like you’d only be able to repay under the new Standard or RAP, even if you have loans from before July 1, 2026.3 While that may help hasten the demise of old plans and loan terms, there are 43 million people out there with loans, and only a relatively small share will borrow again. This means that, for the next 20+ years, you’ll have borrowers using “old” Standard, Extended, Graduated, “old” IBR (old old IBR?), and in the case of Parent PLUS, ICR.

While this may be beneficial to some borrowers, it’s a complexity nightmare for the system. It means that all of those repayment plans need to remain an option in FSA and servicing systems until the last borrower leaves those plans. All of the plans still need to be considered when new programs or policies are created, customer service representatives would need to know the timeframes and terms of these plans to appropriately counsel borrowers, and online tools need to be coded to offer borrowers the right option set depending on when they borrowed. It also means that government websites presenting repayment options need to break people’s brains with an “if this then that” set of instructions for helping borrowers figure out what plans they can enroll in. We see how this plays out on StudentAid.gov today.

While this excerpt from StudentAid.gov may be understandable to the few of us who have been steeped in the bitter waters of the higher education policy space, to find this useful, you have to know A LOT about the loan programs, what loans you have, when you borrowed, if you ever consolidated, what consolidation even means, what “discretionary income” is and how the government defines it in this context, and what you’d pay under whatever the hell the 10-year Standard Plan is.

In conclusion

This is a whole lot to implement. I’m sure there will be revisions in the coming weeks and months that clarify some open questions and that change the terms of some of these programs. I’ll end on this: I cannot imagine how FSA is going to get this done. The bill gives differing timeframes for implementation of these things, with the soonest being 6 months or 270 days (which is probably a typo because they conflict) to move borrowers from SAVE, ICR, and PAYE into old IBR (and maybe also in making RAP available, depending on if current borrowers are allowed to enroll in RAP without consolidating or borrowing after July 1, 2026). One saving grace is providing FSA with $500M per year for the next two years (which is phrased as providing those funds to servicers, but money is, you know, fungible), but still, FSA is half the size it was and still has procurement rules to overcome should it try to bring on new contractors to do some of this work.

More to come on accountability and ED later this week (laughsob). I appreciate you!

The world’s biggest ups to my group chat buds on helping me trudge through this thing. You know who you are <3

This would be most helpful for borrowers who have a lot of debt and high enough incomes that they’re chipping away at principal but not really making a big dent month-to-month.

It is also unclear to me if old borrowers can enroll in RAP if they don’t take out a new loan or consolidate after July 1, 2026, and, if they can, if they can ever switch back to one of the old plans, or if they have to choose between new Standard and RAP going forward.