Simply Unprofessional

The new graduate loan limit debacle and how we're always losing the plot

Most of the time, higher ed policy changes don’t really break through to the broader population. When the higher ed portions of the reconciliation bill went minimally covered by most news outlets, I was pretty surprised given the level of attention (and clicks) anything related to student loans gets. But then one morning, almost two months after negotiated rulemaking ended for the student loan programs ended, I logged onto Instagram to see Dr. Jessica Knurick, a nutritionist whose public health content I often find interesting, covering… student loan limits. Oh no.

The reel uses heavily biased language (“tucked in” the bill - girl it’s on the internet, it ain’t hiding anywhere), includes several factual errors (like the fact that distinguishing “graduate” and “professional” programs is a new thing), and claims that this is a nefarious attack on equity, women, and your health. It’s a great example of how to get people riled up over an issue without relying on the things this creator purports to care about - data, scientific evidence, and appreciation for nuance. The comments expanded on some of the theorizing as to the nefarious motivations of the Trump Administration, policy proposals that leverage with my favorite phrase (“predatory debt”), and lamenting the good ol’ days - you know, from 1965 to 2024 - when higher education wasn’t a luxury.

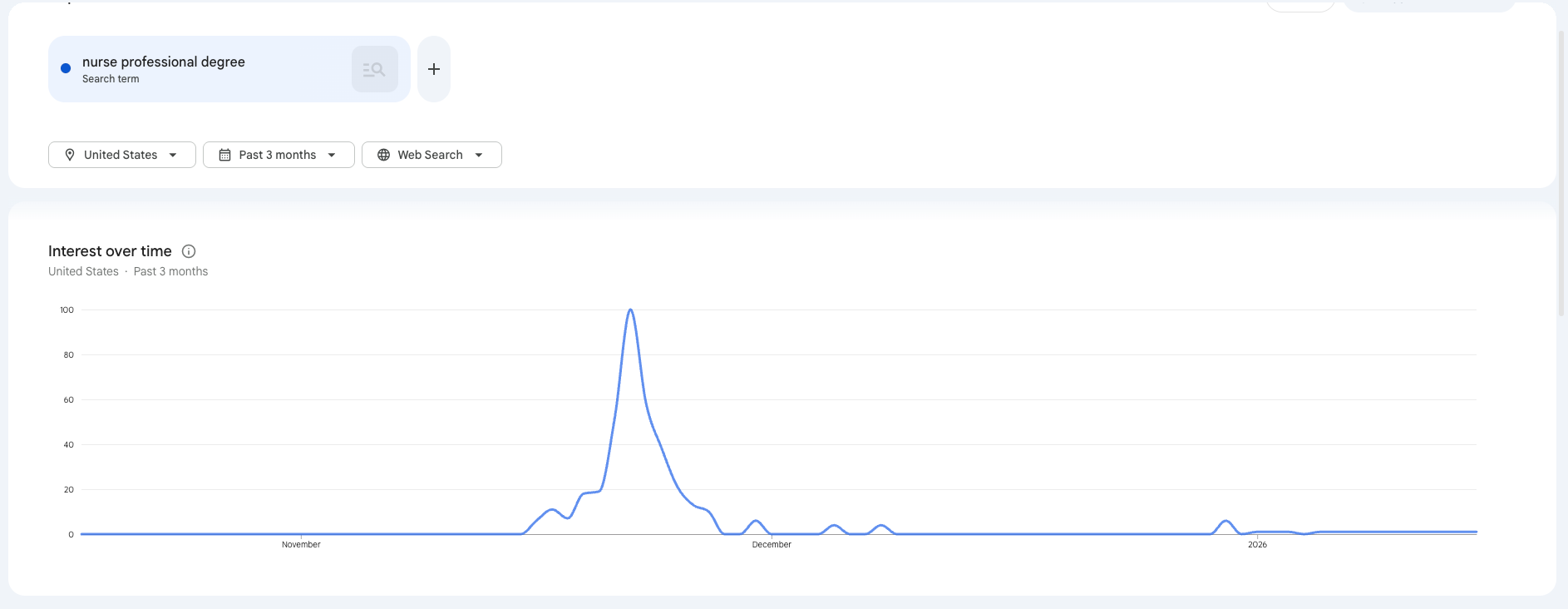

While folks on social media almost always have a really hard time staying in their lane, I find this to especially be in the case for higher education and student loans issues, as many of the people weighing in online have been to college or have student loans, thus making them an expert (duh). The line of “the Trump administration doesn’t think nurses are professionals” really broke through into the mainstream, and there are now pages and pages of results when you search Google, Instagram, or TikTok for “nurse professional degree,” which peaked in popularity the day Dr. Knurick’s reel was posted, on November 21, 2025.

When I posted on my own personal Instagram about the poor framing of this issue, I got pushback saying that some nurses do need a graduate credential (true!) and that the Trump administration should instead be going after the bad schools and programs that are overcharging people. Of course, these folks are not recognizing that OB3 also included accountability for graduate programs for the first time EVER, simply because it went underreported. But I would also hazard a guess that, if framed a particular way (e.g. the Trump administration is going after social work programs - with the below the fold whispering “because we don’t pay social workers enough”) most folks would also buy that program-level accountability is ALSO bad.

What none of these social media posts has mentioned is that there actually was significant discussion and a couple of proposals - put forward by the typically-conservative taxpayer advocates - to include the most common health-related graduate programs (including nursing!) in the set of professional degree programs. While the Department rejected the proposal as too expansive, it was discussed at length. The Trump folks at ED got so annoyed by the hoopla that they published a Q&A on the new regs aimed at breaking through some of the rhetoric, but unfortunately, the administration’s own rhetoric undermines its ability to be a trustworthy arbiter.

I think that fact that this has generated so much noise says a lot about exactly who is loud online - and that many of them are part of just 14% of American adults with a graduate degree. And I’m not saying all of this because I agree with the Department - I actually think it’s extremely short-sighted to not include most health professions in the professional programs list. While I understand not wanting a lengthy list of programs or a definition that could potentially be abused by schools looking to bend the rules to let students borrow more, our heathcare system is not equipped with enough staff, especially as Boomers age and supply-side pressures on providers increase. But the way that we as a society approach policy problems - especially on social media - has become an exercise in polarization, negativity, and conspiratorial thinking that does our mental health and our opportunities for advancing good public policy no good. When we take a conversation about how much debt is an appropriate amount for graduate students to borrow and morph it into the Trump administration doesn’t think nurses are professionals, we’ve devolved to such an extent that so much smog must be cleared from the air before we can get back to a real policy conversation.

“It threatens the diversity, talent, and public-service mission that define our school”

A few other things stood out to me about folks’ outrage around this issue. The first is that most people seem to have forgotten that, just a couple of years ago, we were operating at peak levels of “federal student loans are predatory and they all must be forgiven.” But now, when loans are limited, we yearn for the days when students could borrow as much as they want again. And the second thing that stood out, related to the first, is that very few of the critics of this policy look at higher education as a business, one where many institutions are charging unnecessary premiums for the pleasure of enrolling.

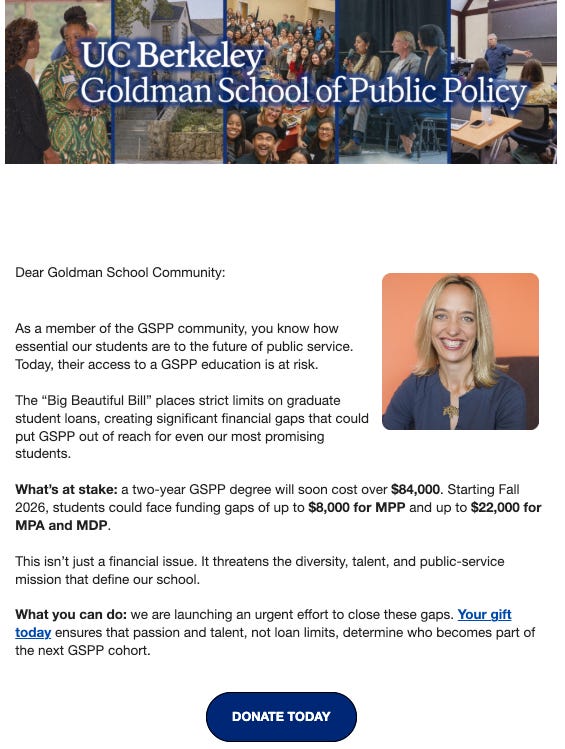

A couple of weeks after the outrage reached its peak, a friend forwarded me this email from their graduate alma mater.

For the record, I have a MPP degree from Michigan and I am very glad that I pursued that program because it helped me build a strong analytical skillset. But you better believe that I would not have enrolled if they were charging me $84,000 to get those skills, and it would be hard to convince me that Goldman is spending anywhere close to $84,000 per year to educate its students.

I find it funny that Goldman sent this plea out to its alumni considering how difficult they make it to understand how much it will cost a prospective student to enroll. The information is as hard to find as I expected. First, I went to their website, which has no clear links to finding information on tuition or financial aid. Perhaps it’s under programs?

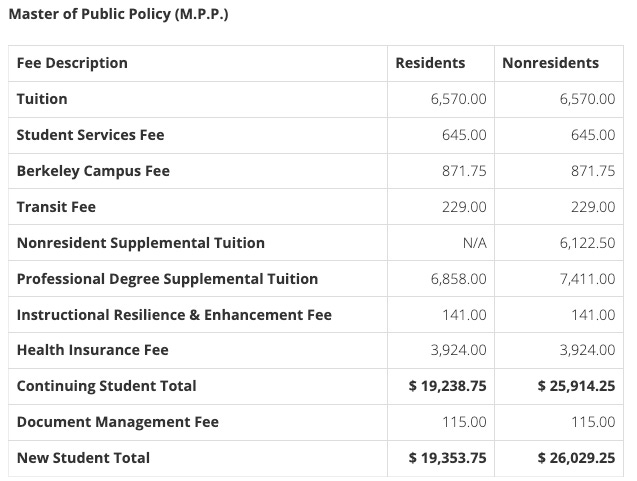

Let’s click Master of Public Policy. From there, we get a sidebar allowing us to look at cost information. But then we get sent to another link.

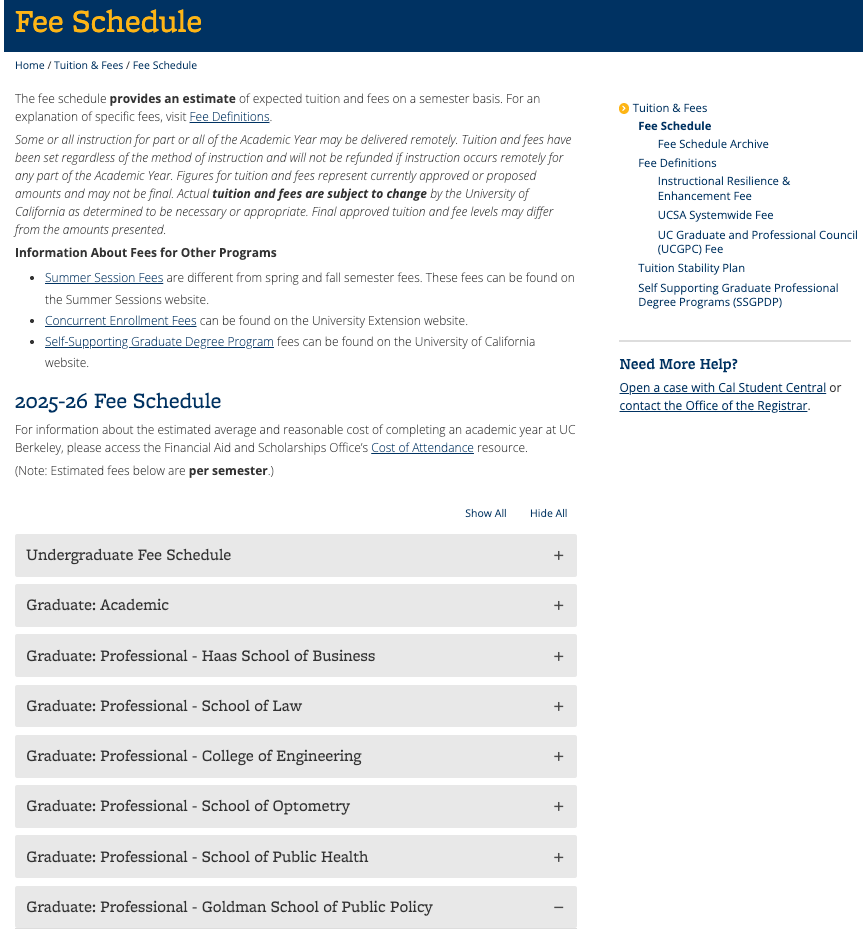

On the registrar’s website, we are left to look down a long list of schools and then programs. We’re exhorted to remember that these figures are an estimate but not that the numbers listed are only for one semester.

This is perhaps my favorite part. There’s no reminder further down the page or in the table that this is ONLY FOR ONE SEMESTER. They also try to make it seem like they charge in-state and out-of-state residents the same amount of tuition by throwing a separate line item for “nonresident supplemental tuition” further down the list, where it’s simply another fee for nonresidents but also quite the deal for residents because hey, one of the list of fees doesn’t apply! Hooray! And they’re being extremely transparent on your expenses, even listing your “document management fee!” The fact that living expenses are nowhere to be found in one of the most expensive metropolitan areas of the country must surely be an oversight… especially considering graduate students used to be able to borrow for living costs, not just tuition and fees. Oh, but what’s this “professional degree supplemental tuition” line?

Turns out, the professional degree supplemental tuition cost was added by UC Berkeley all the way back in 2010 and is basically additional tuition charged by a graduate student’s college to “sustain and enhance program quality.” Interesting. Well, we can now see that Berkeley is charging nonresident students $52,058 per year… so I guess we get to $84K by adding in another $28K in living expenses. Public mission, indeed.

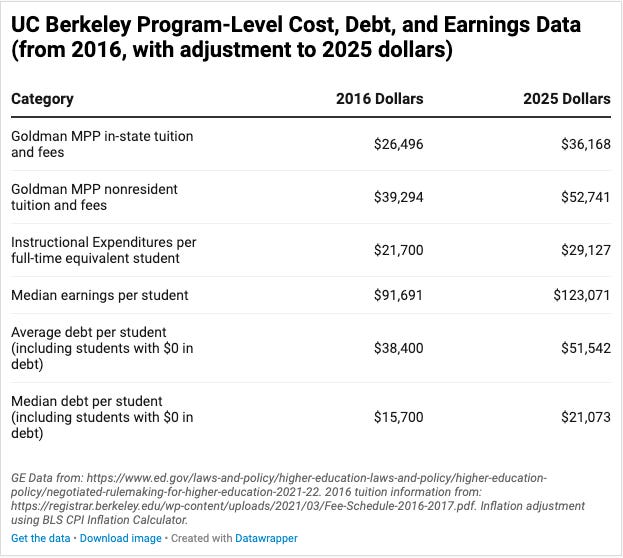

The question of value or return on investment has been a hot topic over the last 20 years or so, and there are a whole lot of ways that we can measure this. Over the last 15ish years, we’ve tried to regulate programs to at least make sure that they’re not burying students in debt without offering commensurate earnings. Some of the data that has been collected and published is, what we might call, illuminating. The table below shows data for the 2015/2016 for Berkeley’s public policy analysis (i.e. MPP) program.1 I’m also showing these figures in December 2025 dollars to help give us better grounding in the present.

What we see here is that, at least in 2016, Berkeley was charging students more than it takes to educate them - and that’s with a measure that represents spending across for every single credit-pursuing student (undergrad and grad) and that IPEDS itself says “may be inflated.”2 What I also see here with this very high average debt but low median debt is that there are some students borrowing a whooooole lot of money to enroll in the MPP program, while there are also many students not borrowing at all or borrowing a small amount. I find it most interesting that the average debt is about the same as the nonresident tuition cost, and I wonder what the distribution of debt looks like for resident and nonresident students, as well as what Goldman’s discount rate is for it’s public policy program.

Now, I’m not saying a Berkeley MPP degree is not of a high quality, or that most graduates aren’t making up for the debt they borrow by increased earnings over their careers. But I do think it’s wild to send an email to your alumni saying that Republicans are putting Goldman “out of reach” for their “most promising students” when they are the ones who made that education so expensive in the first place.

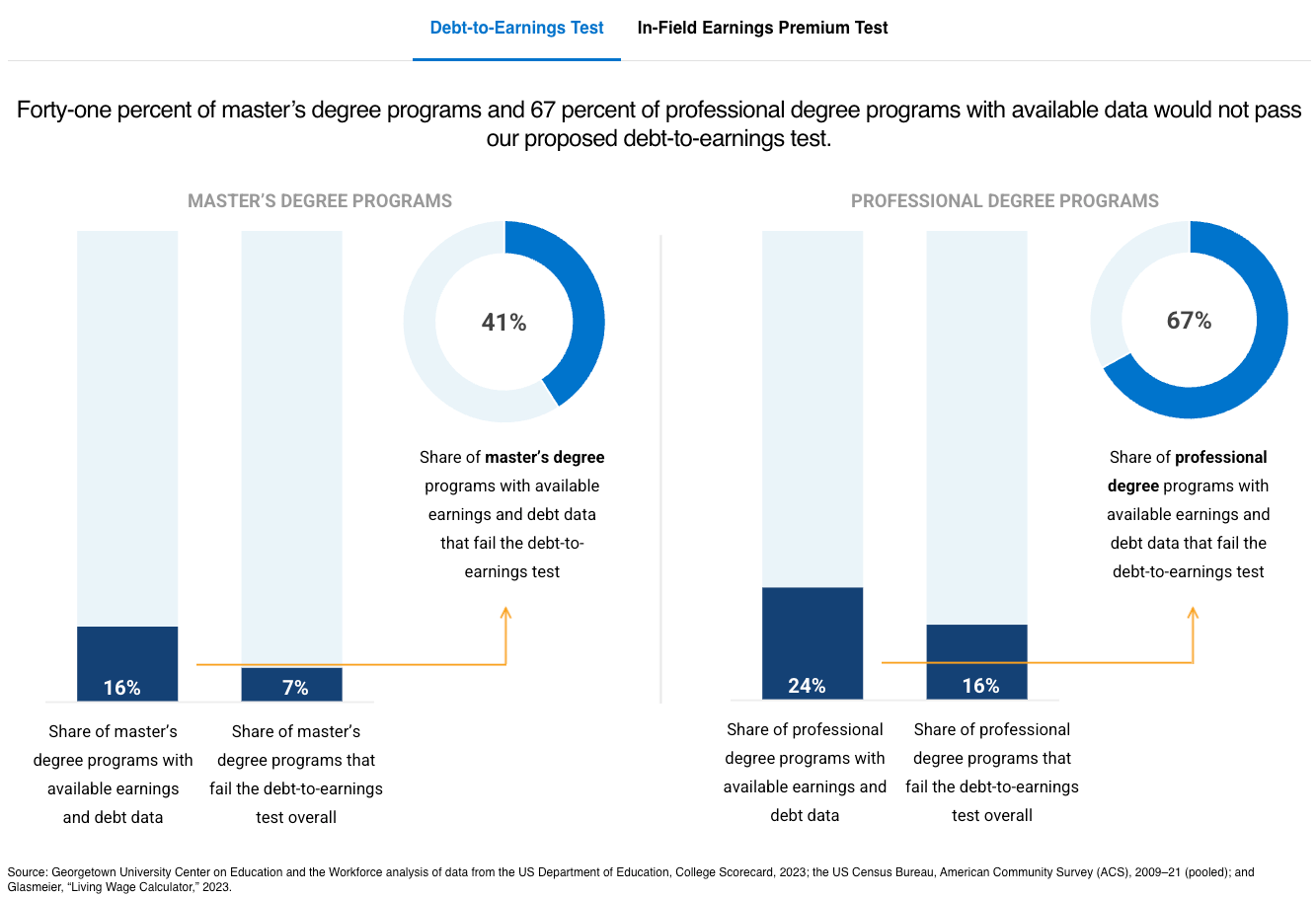

The fact of the matter is that since the Graduate PLUS program started in 2006, colleges have used master’s degree programs in particular to subsidize their operations, offering more and more programs - online, one-year, catered to all kinds of subsets of the working population like “executives” - to get that sweet, sweet Graduate PLUS loan revenue without having to worry about completion rates, earnings or career-placement outcomes, or loan repayment rates. For the most part, colleges had carte blanche to do what they wanted with graduate education and the government looked the other way. An analysis from Georgetown sets a reasonable debt-to-income test - where graduates’ median federal loan payments would need to be less than 10 percent of their median earnings above the state living wage - and demonstrates that 41% of master’s programs and 67% of professional programs with data on file would fail that test.

But now that loan limits and accountability standards3 are imminent, colleges get to stand back and let people on social media fight for them, simply because its happening during the Trump administration. The dirty secret in Washington is that Democrats have been critical of the excesses of graduate programs for several years, but don’t have the wherewithal to fight with the colleges or be painted by those further left of them as an enemy of public colleges or diversity or equity or whatever other hot phrases folks want to toss around. After all, with the depths of partisanship that we’ve fallen to, one accusation could paint you as a traitor of whatever cause for the rest of your career.4

Congress? Reacting? No Way.

The flurry of online outrage about this patent discrimination against women and mandatory reporters has led lawmakers to show their constituents that they are willing to fight for their right to borrow a ridiculous amount of debt with zero guardrails to protect them against bad programs. The bill that has the most momentum is from Mike Lawler (R-NY) whose bill expands the list of professional degree programs to include nursing (duh), physical therapy, clinical psychology, physicians assisting… and education, ministry, and social work, among others. This would expand loan limits from about $20K to $50K per year for these fields. Never to be outdone, a few democrats have put forward their own bills that take broader approaches, delaying the Grad PLUS loan limits until 2030 (fingers crossed Dems with the presidential in 2028, amirite), raising the graduate limit for all programs to $50K, or dumping loan limits for graduate and professional programs altogether.

But I think it’s prudent for lawmakers to sit back and see how this plays out. Some good data from Preston Cooper shows that nurses are not, in fact, going to be broadly hurt by the bill, schools are starting to announce new grants to make up for limited loans, and states are exploring their own loan programs. I think it’s pretty clear that unlimited borrowing was not good, and that, even though women and racial minorities have pursued graduate education to level their salaries with their white male peers, they have done so at the expense of their time and debt burden. Maybe we should be trying to address labor market issues through labor policy rather than trying to solve every problem by turning the dials on student debt.

This was a long one that’s been in the hopper for awhile, so I appreciate y’all’s patience and your eagerness for more posts. TTFN.

Unfortunately we don’t have all of this data for a more recent year because GE had, um, kind of stalled, but hopefully we’ll get to see more at some point in the future.

See the note on figure 17 on page 7. https://nces.ed.gov/ipeds/DataCenter/DfrFiles/IPEDSDFR2016_110635.pdf

As a reminder, graduate programs must now show that working completers earn more than the median bachelor’s degree recipient in their state.

Ask me how I know.